As we are gearing up for the holiday season, I have found myself reflecting on 2011. It was a fantastic year for ID Insight and we can't wait for 2012. While there were many great memories on the business front, there were as many or more on the life front. Here is my top 10 list for 2011.

- Continued growth. ID Insight continued to see significant growth for the third year in a row. We concluded our 9th year in business by adding many new clients, retaining our existing clients and creating new products and enhancements. Giddy about what we can and will do next year.

- Time at the Lake. I feel blessed to have been able to spend some serious quality time at the lake this summer with my family, parents, in-laws and friends. Lots of boating, swimming, camp fires and fishing. Looking to resume when the snow melts... probably in May.

- Partnerships. We are fortunate to have established great partnerships with FIS, Fiserv, First Data and others. We enjoyed continuing to develop and grow these relationships. In 2011, we also fostered new partnerships with Centris, Zoot and others. While our business drives these partnerships, I am most thankful for the people and personal relationships that have been developed.

- Football. While football has always been a part of the Elliott family, it took a turn this year when my 9 year old daughter Abby decided she wanted to play tackle football with the boys. Things were interesting at times, but by year end she was having a blast and is now preparing for next year's season.

- Twin Cities. After spending 3 years driving 120 miles round trip, we were all extremely excited to move our corporate office back up to the Twin Cities. Our employees have become much more efficient and able to spend more time with family and friends. Fantastic.

- Coaching U8 Girls Hockey. I decided to become head coach of Abby's U8 Girls hockey team this year. It has been an absolute 'gas'. Smiles everywhere and they actually listen. One of the most rewarding experiences I have ever had.

- Broadband Scout. A break-out year, where we added many of the top broadband issuers in the country, Federal, state and local government and various other groups. We topped our 500 millionth transaction as well.

- Travel. Kelly loves to travel and we were fortunate to get a few trips in this year. We got out of the snow to see family in Arizona in March. We also enjoyed a few days in the Florida Keys in April with friends and were back at Disney World in the fall. All great memories and able to warm our Minnesota bones.

- Our employees. We added to our team this year, accomplished a ton and had fun doing it. We were excited to bring on Sudheer as our senior engineer, Lee as a Data Analyst and somehow coerced my beautiful wife Kelly to join as our Office Manager. Our company is our employees and I couldn't be more proud.

- Duck Hunting. After a couple years away from the duck blind, I was dragged back this year by young Abby who begged long enough for her first duck hunt that Dad capitulated. We hunted for an hour and nearly got our limit of mallards. She now think duck hunting is going out for an hour in nice weather and getting your dinner. I resisted the urge to take her back out a week later when the temperature dropped to single digit.. maybe next year.

Anyway, I am thankful for 2011 and greatly looking forward to 2012. Here is wishing you a great work / life balance, a fantastic holiday season and a prosperous 2012!

Friday, December 23, 2011

Thursday, September 22, 2011

Where is all of this Analytics Stuff Going?

Over the past few months I am increasingly intrigued by what has been going on in the field of analytics. Over the past couple of decades, the word "analytics" has been fashionable. Whether it was text-mining, web analytics, CRM, neural networks, etc. the word analytics has become a standard word in our business language and required for nearly any job qualification these days.

While analytics has been fashionable for awhile, there are certain driving forces lining up that I believe are going to drive analytics to levels never seen before. This explosion can be attributed to the sheer explosion in data volumes available for analysis and the vast storage and instantaneous retrieval to make more informed decisions much faster. This trend is only going to continue.

We are already seeing this beginning to accelerate with the crazy amount of acquisitions going on over the past couple of years. IBM alone has acquired Netezza ($1.7B), Unica ($.5B), SPSS ($1.2B), and most recently i2 and Algorithmics ($.4B). And it doesn't end with IBM: HP came out in August and said it was going to be exiting the PC and tablet market, and then bought Autonomy for $10B to focus on .... you guessed it: Analytics. These are not sporadic, small plays. They are massive, industry changing moves.

And it doesn't matter what industry you look to. Counter-Terrorism, banking, advertising, health care. Everywhere we look, the data is exploding exponentially creating the biggest sandbox of questions and answers ever seen. For example, companies are now developing analytic technology to know where I use my android smart phone and when. Imagine you are walking out of your office at noon for lunch when an advertisement comes across your phone with a 20% coupon for the restaurant across the street. Talk about relevant.

Speaking of smart phones, the long promised notion of mobile payments is quickly taking shape. The technology pieces are finally aligning and we are seeing some major moves from the big payment providers (Visa, Mastercard, Amex, Google) in this direction. The crusty old bank payment channels are being attacked on all fronts. What has me completely mystified is what will happen when this analytics explosion collides with the explosion in mobile.

I am going to grab my box of popcorn, and and get a good seat for this show.

While analytics has been fashionable for awhile, there are certain driving forces lining up that I believe are going to drive analytics to levels never seen before. This explosion can be attributed to the sheer explosion in data volumes available for analysis and the vast storage and instantaneous retrieval to make more informed decisions much faster. This trend is only going to continue.

We are already seeing this beginning to accelerate with the crazy amount of acquisitions going on over the past couple of years. IBM alone has acquired Netezza ($1.7B), Unica ($.5B), SPSS ($1.2B), and most recently i2 and Algorithmics ($.4B). And it doesn't end with IBM: HP came out in August and said it was going to be exiting the PC and tablet market, and then bought Autonomy for $10B to focus on .... you guessed it: Analytics. These are not sporadic, small plays. They are massive, industry changing moves.

And it doesn't matter what industry you look to. Counter-Terrorism, banking, advertising, health care. Everywhere we look, the data is exploding exponentially creating the biggest sandbox of questions and answers ever seen. For example, companies are now developing analytic technology to know where I use my android smart phone and when. Imagine you are walking out of your office at noon for lunch when an advertisement comes across your phone with a 20% coupon for the restaurant across the street. Talk about relevant.

Speaking of smart phones, the long promised notion of mobile payments is quickly taking shape. The technology pieces are finally aligning and we are seeing some major moves from the big payment providers (Visa, Mastercard, Amex, Google) in this direction. The crusty old bank payment channels are being attacked on all fronts. What has me completely mystified is what will happen when this analytics explosion collides with the explosion in mobile.

I am going to grab my box of popcorn, and and get a good seat for this show.

Monday, August 1, 2011

Where is My Broadband Connection?

Over the past few months and quarters the notion of where my broadband connection resides has shifted...... at least for me. A few short months ago, I would have told you that my broadband provider was Comcast, as that was who provided internet access to my home.

A few short months later, I am not so sure. A few months ago, I bought one of those funky new Android smart phones on Sprint's 4G network. I am now seeing download speeds of 3-6 mbps that exceeded my basic Comcast cable connection that was coming in around 3 mbps.

What is more interesting to me is the Android comes with me wherever I go. Whether I am at the lake, work, the store or the coffee shop - my internet is there with me. On occasion, my wife will ask me to turn on the "hot spot" so she can connect in with her iPad.

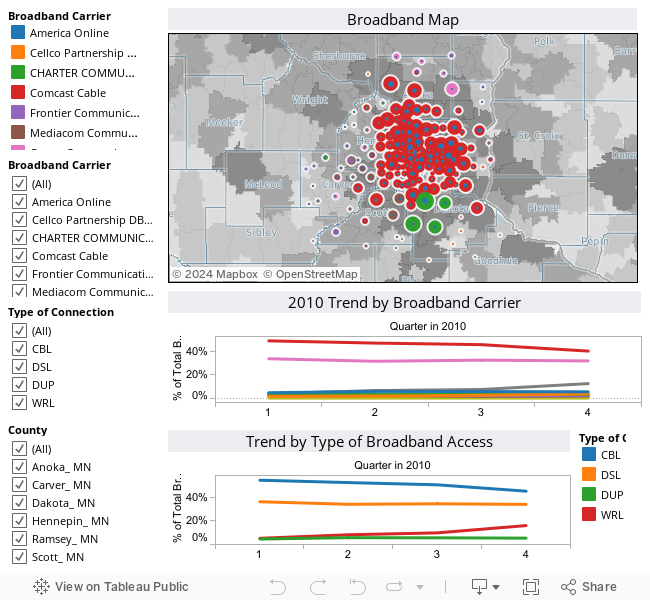

To see what was going on with wireless internet versus traditional broadband, we turned to Broadband Scout and looked at what was going on in the Twin Cities 7 country metro. Specifically, we looked at all of the major providers and analyzed the trends or changes that have occurred over the past few quarters. What we found was that internet transactions through a wireless device increased by a factor of over 200%, whereas Cable and DSL diminished by a few percentage points.

These trends and others can be seen below on our interactive map. Feel free to select various types of broadband providers or the providers themselves to see what is going on in the Twin Cities area.

A few short months later, I am not so sure. A few months ago, I bought one of those funky new Android smart phones on Sprint's 4G network. I am now seeing download speeds of 3-6 mbps that exceeded my basic Comcast cable connection that was coming in around 3 mbps.

What is more interesting to me is the Android comes with me wherever I go. Whether I am at the lake, work, the store or the coffee shop - my internet is there with me. On occasion, my wife will ask me to turn on the "hot spot" so she can connect in with her iPad.

To see what was going on with wireless internet versus traditional broadband, we turned to Broadband Scout and looked at what was going on in the Twin Cities 7 country metro. Specifically, we looked at all of the major providers and analyzed the trends or changes that have occurred over the past few quarters. What we found was that internet transactions through a wireless device increased by a factor of over 200%, whereas Cable and DSL diminished by a few percentage points.

These trends and others can be seen below on our interactive map. Feel free to select various types of broadband providers or the providers themselves to see what is going on in the Twin Cities area.

Wednesday, November 10, 2010

Positioning Product With a Sledge Hammer

I continue to be amazed at how sensitive the sales engine can be to your product positioning. After all - the product is the same functionality with the same general need, price and value. However - over the past few years our product positioning has changed fairly drastically. Much of this change in positioning has been due to market conditions and market needs. What I have learned is that you need to be constantly aware of your product positioning and how market conditions can impact that positioning.

In 2003, we created Safe2Change to be the preeminent solution to screen address changes for the possibility of identity theft. In positioning the product, our key messages focused on "taking a bite out of crime" and "stop the fraud losses". While that all sounded good, it didn't really end up with us taking the world by storm. At that time, identity theft was quickly becoming a national story. Identity Theft was hot - and we felt our positioning was well suited for those market conditions.

Unfortunately - while the topic was "hot", our customers weren't buying into it. Why? Because, even though it was a hot topic, our typical client was not being impacted by the rise in identity theft in a meaningful way.

Flash forward a few years to 2008 and the marketplace changed again. Identity theft was still relatively hot, but in late 2007, the FTC came forward and mandated that by November of 2008 that all financials institutions needed to screen address changes to meet the new FACT Act compliance standards. Suddenly, we changed our positioning from "stop the fraud" to "Safe2Change is the most cost-effective way to meet compliance".

It was a good move and allowed to us to bring up over 500 banks prior to the compliance deadline. However, I don't think it was necessarily our product positioning that drove that response. The reason most bought was purely out of fear. They had to do something and Safe2Change was available.

While we did bring up more than 500 institutions, that only meant that about 20,000 chose something else, and for the lion's share - these institutions chose to send first class letters to consumers who changed their address as their compliance solution.

Once this was adopted in late 2008, the last thing the banks were thinking about in 2009 was changing to something else. In 2009, I think we were most interested in trying to find a cave to hibernate in. Banks were not interested in changing solutions and didn't have the resources to change anyway.

As we entered 2010, suddenly we saw logic and rationality return to our clients and prospects. Further, our clients began to realize how painful their letter mailing compliant solution really was. As we got deeper into things, we also realized how ineffective that a letter mailing strategy is. In short - it is expensive, inefficient and a bigger problem than people first realized.

As such - we once gain found ourselves evaluating the positioning. We had gone from "stop fraud" to "best compliant solution". While those strategies may have made sense for the market dynamics at the time, it was no longer top of mind. Suddenly - it was all about cost and expense.

We quickly shifted gears and focused on cost as our main positioning. Why? Well, as someone once put it "It's the economy stupid". We realized that while banks were spending needless dollars on expensive manual processes, it was not until recently that this number began to become meaningful. Suddenly saving half of postage fees for a year means I don't have to cut 3 more headcount.

This new positioning is now paying dividends. Since adopting this, it has become our sledge hammer. Are you interesting in saving millions of dollar sounds pretty good. This positioning in 2003 or 2008 did not have any meaning. Now it does. It is generally the same product, the same general needs with the same pricing - but the positioning has changed to meet the changing market need.

Kleenex would have been a lot easier.

A.E>>>

Tuesday, October 5, 2010

The Need for Speed

The ability to go "faster" is part of the culture of the United States. Whether it was moving from the horse and buggy to the automobile, the prop plane to the jet engine or moving from dial-up internet service to broadband, we are always looking to do things faster.

And every time we make a monumental leap in speed, economic prosperity springs eternal. While the tangible benefits are many times obvious, it is the intangible benefits that are more interesting to me. For example, when we moved from horse and buggy to the car, people were hired to make the cars. Likewise, steel became much more important which led to economic booms in towns like northern Minnesota and the steel belt. However - it was the intangibles that became interesting. This economic boon created tons of new jobs, which in turn led to the creation of many other innovations and industries such as the airline industry. It also created the need for highways and byways, reductions in cost and increases in trade.

We saw a similar phenomenon during the dot com era. Heading into that period, it was as if we didn't have any idea what would be the end result. Amazon, online bill pay, PayPal, Google, etc... How could one predict all of what would happen by allowing people to connect to one another. This was pushed one step further when we moved from dial-up to broadband.

Flash forward a few years and here we are again. For the past decade, we, as consumers, have been rather content with our internet and current broadband speeds. The lay consumer will tell you that their broadband speed is "OK" and when you ask them what speed they are getting, the normal answer is "I don't know".

Today in the U.S., the average consumer with cable broadband is getting roughly 5 megabits per second of download speed and 2-3 mgbs of upload speed. This metric describes how much data you can download or upload over that connection. DSL, wireless and satellite connections are less than cable on average.

We are now at the forefront of what appears to be a broadband war. The broadband stimulus program is in full swing with billions of dollars having already been awarder to bring high speed broadband to the nation. Where this is all heading is not yet known, but the theme is the need for speed. Today the U.S. ranks in the 20's as a nation on the broadband speeds given to consumers. Meanwhile, there are countries such as Singapore where the entire country is getting speeds of 1 gigabit. That's right - speeds about 200 times what we receive today on average.

As we begin to move up the speed ladder, the most immediate benefits are fairly clear. We can get information faster. We can do things like watch TV (think advertisement) on our mobile devices. We can transfer very large online medical records in a flash.

However - it is those intangible benefits that are most intriguing. What other value chain items will be positively impacted?. What new technologies and innovations are going to be created? What new payment methods and trade will this enable? How will this re-vitalize rural areas that have not been able to participate in the global marketplace?

Will this next jump in speed lead to the economic springboard that we have seen in the past? If we truly do substantially improve our broadband infrastructure and speed, my answer is going to be YES. The other important question is whether the U.S. will move up the ladder or let about 22 other countries that are ahead of us reap the benefits.

Friday, June 4, 2010

From Pipes to Platforms

As we look at fraud detection systems for financial services, it gets very interesting when we consider what has emerged. Here is a snapshot of what we typically see:

- New fraud trends routinely pop up. (Think phishing, bust-out, takeover, new account, etc..)

- When the problem becomes big enough, the institution seeks out a solution to identify this fraud. This is typically a point solution that solves for that specific problem.

- As new types of fraud emerge, the next point solution is deployed.

- Many of these solutions are dependent on data and analytics.

- Over time, we begin to see a maze of overlap with respect to data and functionality.

- Suddenly, we find ourselves with a highly complex system.

- In addition, our cost to administer and manage the growing list of vendors increases.

So how do we end the madness? How do we meet the business needs most optimally?

How do stop the fraud, anticipate the next fraud type and not significantly increase the costs of creating such a complex system?

I think the answer lies in both the data and the technology choice. On the data front, we routinely see clients with many data solutions all of which overlap highly. It is not uncommon for us to see clients with 5-10 separate point solutions or more. They have ID Insight for this, Lexis for that, Experian for this doo-hickey, FICO for that gidget, etc...

However - when you back away from the whiteboard, we suddenly realize that each solution is bringing overlapping data to a separate, specific solution. Whether it be credit bureau information, utility records, etc., we see that these solutions are utilizing very similar or even the same third party databases. This should not really be a suprise, as most solution providers are all going to the same root data.

The end result is a system that connects to many very specific point solutions. The typical solution is very rigid. That is, "our solution looks like this and this is how you connect". Suddenly, we have 8 or 10 rigid pipes, all of which share many of the same components.

So back to ending the madness. In a Utopian world, I would have all the data I need at my disposal in one pipe, and this pipe would not be rigid, but flexible tubing with connections to bring in even more information and data. From a solution side, this utpoian view would also allow me to use the raw data and information to solve for any future fraud types that emerge.

So while today my problem may be takeover, it might be something entirely different next week. Rather than have to go out and find another rigid pipe - why not go to my flexible pipe and just ask to solve for the problem? Under this view, I suddenly realize the enormous benefits:

- I don't have to through an RFP to identify the "best" point solution.

- I don't have to wait for months (and sometimes years) to solve. I can turn it on immediately and stop the bleeding.

- I can also turn certain features off allowing me to reduce cost.

- I don't have to manage another vendor and bring another through the Security hurdle.

- I get to sleep at night realizing if something new emerges, I am now equipped to stop it quickly.

We see this Utopian view emerging over the next few years. The madness cannot continue and the various consumer, cost, security and compliance pressures are forcing this.

What we see is moving from the world of rigid pipes to what is becoming known as "Platform as a Service". Rather than point solutions, we will move to data and analytic platforms that are flexible and able to react very quickly.

Here are the high level compents of what we see in the future Fraud Platform.

- Will have the most comprehensive set of data to solve for 90% or more of all existing and anticipate fraud problems.

- The ability to quickly bring in more data as needed.

- The ability to ask for any data desired for whatever reason.

- The ability to customize your treatment of the data (eg. I want a tight or loose match on address, while I want an exact match on Social security number).

- Have multiple modules or components that can be turned on or off as desired. Eg. a bust-out module, a custom score, a takeover module, etc..

- An easy to use web-anabled dashboard that allows the client to quickly and efficiently enable data, solutions, modules, etc...

We recently launched the next version of CompleteID and in doing so, enabled users to do many of these things. Customize scores, alter rules, changing matching criteria, customize data sources, etc.

This is already resulting in many new customers. While solving for the immediate problem is necessary, clients realize the power of being able to have a flexible system that can react quickly.

Stay tuned as we continue to remove the rigid pipes and move to the Platform.

A.E>>>

Friday, April 23, 2010

Arkansas is the Most Competitive BroadBand State. Huh?

Yesterday, we launch our most recent research report proclaiming that Arkansas topped our list as the most competitive state in terms of broadband internet. Likewise, Rhode Island took up the last spot. Here is a link to the release and the accompanying research report.

http://www.idinsight.com/news/p_04222010.asp

As most in the broadband community know, the debate around competition and competitive markers is heating up. The FCC is deeply interested as are the providers as should all consumers. After all, as Americans we believe in a free market economy and vibrant competition.

That is why we felt compelled to take a deep look at this issue with respect to what the data tells us. We spent over 4 months analyzing the data and having many late night skull sessions discussion the findings and maybe more importantly "what constitutes competition?"

In the few hours that have transpired since launching this report into the cyber world, we have already received a lot of feedback - some good, some bad. I welcome all feedback as it is a very worthy debate and makes us think.

As you look at competition, I would say most have gravitated towards a definition that says "Competition is present when consumers have multiple choices". One recent publication came out and said that 95% of all U.S. housholds have access to at least 4 broadband choices. The conclusion is that for the most part we are competitive.

For us, as we discussed, we began to question that definition. For example, in the Twin Cities, it is very well known that Comcast is to premier cable provider while Qwest is the dominant DSL provider. When you look a layer deeper, you will see some other providers present - but are they really competitive? You certainly never hear of them on the commercials and my mailbox is not being bombarded by direct mail ads to sign up for Hickory Tech. I know there are wireless and satellite services probably, but I am sure most do not think about that.

In addition - things like pricing, speed, customer service definitely impact competition. With that being said, we adopted the most standard definition of Competition. Of course, we can find on Wikipedia. And here it is:

In economics, perfect competition occurs in markets in which no participant has market power. Because the conditions for perfect competition are strict, there are few if any perfectly competitive markets. Nonetheless, the concept of perfect competition can serve as a useful benchmark against which to measure real life, imperfectly competitive markets.

I think that most could at least look at that definition and say it is logical. In fact - it is the standard in economics. After much head scratching - we went with the standard. From a data stand-point, this then says that the most competitive states are the ones where markets powers are not present and multiple viable competitors are present.

To come up with our metric, we basically said the following. In a Perfect Competitive Market, the top providers would have equal market share. To determine that Perfect State, we assumed the following:

- We looked at the top 10 providers in each state.

- We then said it was Perfect if all top 10 providers had 10% market share each.

- We then measured each state's actual market share for the top providers against perfect.

The more that a states actual market share drifted away from Perfect - the lower they ranked. The more they resembled the Perfect Market conditions described above the higher they ranked.

After this measurement and ranking process, we can then look at the data. And when we do, the rankings begin to make sense. For example in Arkansas, there are 6 providers that have greater than 10% market share. However, we observe that in Rhode Island the top 2 providers command 95% of the market and the rest are in low single digits.

If you accept that definition of competitive markets, then it becomes very interesting to analyze the characteristics of states that rank high and those that rank low. In doing so - we observed some startling observations.

First of all, we saw a very definitive trend that showed that as the average income and home values increased for a state, that competition went down. Likewise, as the percent of people using the internet increased, competition went down.

Stepping back and thinking about that raised some very interesting thoughts. In short - the most lucrative markets tend to have fewer large market players. This seems to make sense to me. Eg. you tend to see Qwest in certain markets and Verizon in certain markets, but not a lot of overlap. Why? I am not a network infrastructure expert, but it would seem that as a particular provider comes into a market and builds out their infrastructure over a number of years that is difficult from someone to come in and do the same thing in a much shorter amount of time.

To me - this is where it gets really interesting. Broadband is infrastructure much like it was with roads, schools, airlines, telephone, etc.. And it appears that we are heading down the same path with broadband. Today, we see only a handful of airlines. However - every time I fly, I know that I at least have choices and can go to Expedia to see where I can get the best price. Likewise, with phone, I now have reasonable choices such as cell phones, VOIP, local phone companies, etc...

But what about broadband? If we are truly moving to 100 mgbps or 1 gbps of speed, and the only way this can be delivered is Fiber, and we think back to the competition debate above, it makes me wonder. Will we have choices in the years to come or will we be creating even less competitive markets? I am not sure, but I sure am curious.

A.E>>>

http://www.idinsight.com/news/p_04222010.asp

As most in the broadband community know, the debate around competition and competitive markers is heating up. The FCC is deeply interested as are the providers as should all consumers. After all, as Americans we believe in a free market economy and vibrant competition.

That is why we felt compelled to take a deep look at this issue with respect to what the data tells us. We spent over 4 months analyzing the data and having many late night skull sessions discussion the findings and maybe more importantly "what constitutes competition?"

In the few hours that have transpired since launching this report into the cyber world, we have already received a lot of feedback - some good, some bad. I welcome all feedback as it is a very worthy debate and makes us think.

As you look at competition, I would say most have gravitated towards a definition that says "Competition is present when consumers have multiple choices". One recent publication came out and said that 95% of all U.S. housholds have access to at least 4 broadband choices. The conclusion is that for the most part we are competitive.

For us, as we discussed, we began to question that definition. For example, in the Twin Cities, it is very well known that Comcast is to premier cable provider while Qwest is the dominant DSL provider. When you look a layer deeper, you will see some other providers present - but are they really competitive? You certainly never hear of them on the commercials and my mailbox is not being bombarded by direct mail ads to sign up for Hickory Tech. I know there are wireless and satellite services probably, but I am sure most do not think about that.

In addition - things like pricing, speed, customer service definitely impact competition. With that being said, we adopted the most standard definition of Competition. Of course, we can find on Wikipedia. And here it is:

In economics, perfect competition occurs in markets in which no participant has market power. Because the conditions for perfect competition are strict, there are few if any perfectly competitive markets. Nonetheless, the concept of perfect competition can serve as a useful benchmark against which to measure real life, imperfectly competitive markets.

I think that most could at least look at that definition and say it is logical. In fact - it is the standard in economics. After much head scratching - we went with the standard. From a data stand-point, this then says that the most competitive states are the ones where markets powers are not present and multiple viable competitors are present.

To come up with our metric, we basically said the following. In a Perfect Competitive Market, the top providers would have equal market share. To determine that Perfect State, we assumed the following:

- We looked at the top 10 providers in each state.

- We then said it was Perfect if all top 10 providers had 10% market share each.

- We then measured each state's actual market share for the top providers against perfect.

The more that a states actual market share drifted away from Perfect - the lower they ranked. The more they resembled the Perfect Market conditions described above the higher they ranked.

After this measurement and ranking process, we can then look at the data. And when we do, the rankings begin to make sense. For example in Arkansas, there are 6 providers that have greater than 10% market share. However, we observe that in Rhode Island the top 2 providers command 95% of the market and the rest are in low single digits.

If you accept that definition of competitive markets, then it becomes very interesting to analyze the characteristics of states that rank high and those that rank low. In doing so - we observed some startling observations.

First of all, we saw a very definitive trend that showed that as the average income and home values increased for a state, that competition went down. Likewise, as the percent of people using the internet increased, competition went down.

Stepping back and thinking about that raised some very interesting thoughts. In short - the most lucrative markets tend to have fewer large market players. This seems to make sense to me. Eg. you tend to see Qwest in certain markets and Verizon in certain markets, but not a lot of overlap. Why? I am not a network infrastructure expert, but it would seem that as a particular provider comes into a market and builds out their infrastructure over a number of years that is difficult from someone to come in and do the same thing in a much shorter amount of time.

To me - this is where it gets really interesting. Broadband is infrastructure much like it was with roads, schools, airlines, telephone, etc.. And it appears that we are heading down the same path with broadband. Today, we see only a handful of airlines. However - every time I fly, I know that I at least have choices and can go to Expedia to see where I can get the best price. Likewise, with phone, I now have reasonable choices such as cell phones, VOIP, local phone companies, etc...

But what about broadband? If we are truly moving to 100 mgbps or 1 gbps of speed, and the only way this can be delivered is Fiber, and we think back to the competition debate above, it makes me wonder. Will we have choices in the years to come or will we be creating even less competitive markets? I am not sure, but I sure am curious.

A.E>>>

Subscribe to:

Posts (Atom)